The following are excerpts from a recent Lument report.

by Mike Hargrave and Orin Parvin

The year 2021 was supposed to be all about recovery for the healthcare market, especially for the seniors housing and skilled nursing sectors, and in many ways it was: Facilities reopened, occupancy rates climbed, and processes were improved. The progress, however, was coupled with continued operating challenges as a result of the COVID-19 pandemic and the emergence of variants, as well as rising costs due to labor shortages, all of which have had a stalling effect on the industry’s recovery. The outlook is complex and fluid, and to get a sense of where things are headed, we take a look at recent market data to shed light on the past 12 months, identify trends, and provide a big picture analysis of what the industry looks like as 2022 unfolds.

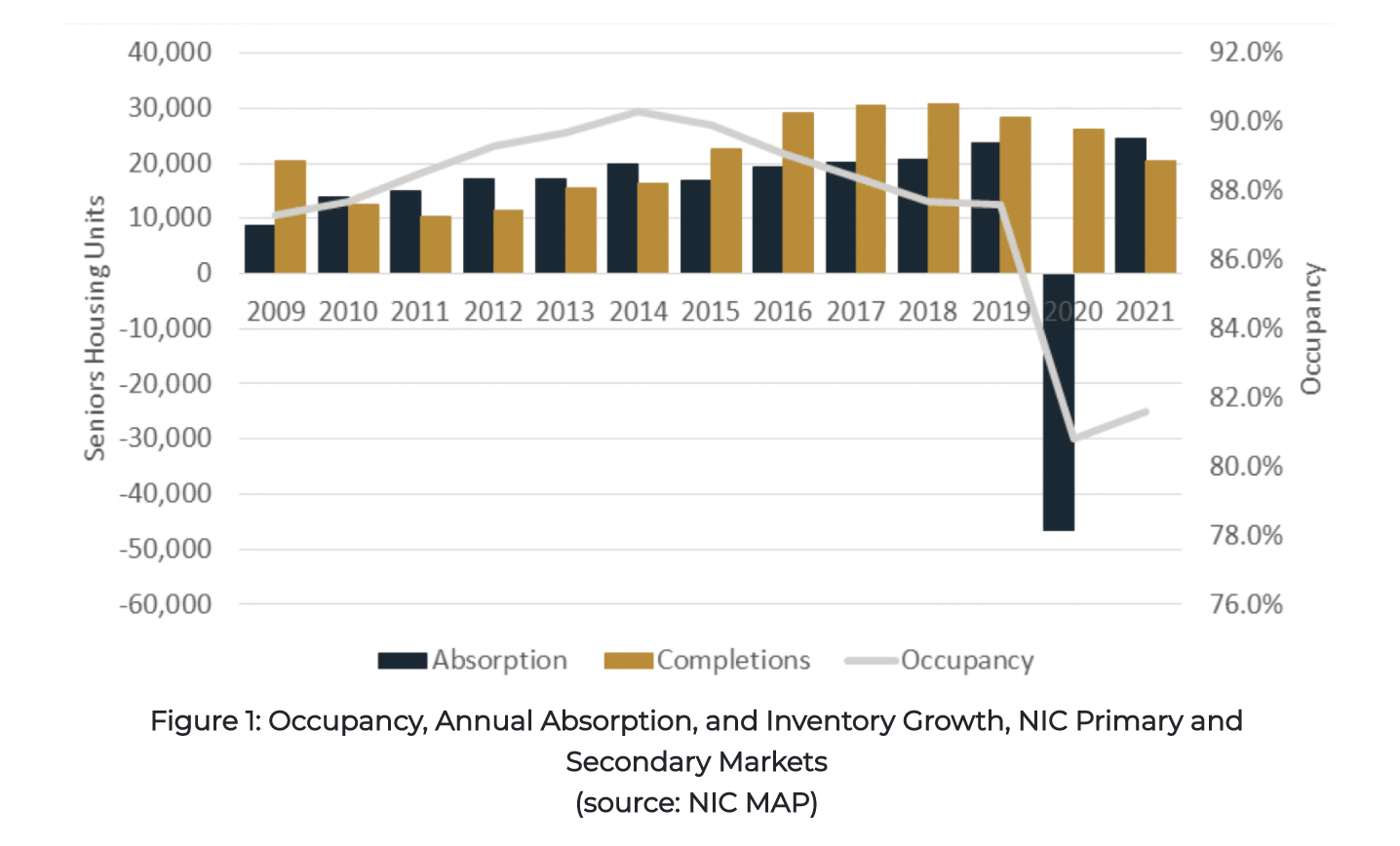

Seniors Housing Occupancy begins the Road to Recovery

Within the seniors housing sector, the occupancy rate reached an inflection point in 2021 and began rising from lows set in 2020. Fueling the occupancy rate rise was record absorption (the change in occupied units) of over 24,000 units in 2021. While the occupancy rate is still low and has a way to go to reach pre-pandemic levels, the turnaround in 2021 was welcome news to many industry participants.

Welltower noted many bullish trends facing its portfolio and the seniors housing industry in general, such as rising occupancies, positive move-in trends, fewer expected forward seniors housing construction volume concerns, and the imminent accelerating growth rates of the 80+ population within the U.S.

As 2022 progresses, we can expect further occupancy gains for seniors housing operators. The tailwinds noted above are imminent and substantial and should help mitigate continuing challenges posed by emerging COVID variants.

Average Monthly Rent and REVPOR Hold Steady

Average monthly rent (AMR), rent growth, revenue per occupied room (REVPOR), and REVPOR growth all performed well in 2021. AMR and REVPOR should continue to improve in 2022 as rising occupancy rates should provide operators with further pricing power.

Occupancy Rises Across Skilled Nursing

The skilled nursing sector also registered occupancy gains in 2021. As we move into 2022, the skilled nursing sector should see further stabilization despite a continuingly challenging operating environment. In December 2021, the U.S. Department of Health and Human Services (HHS) began releasing Phase 4 of provider relief funds, which should help buoy skilled nursing facilities’ (SNF) balance sheets, especially those smaller providers which may be experiencing the greatest operating challenges.

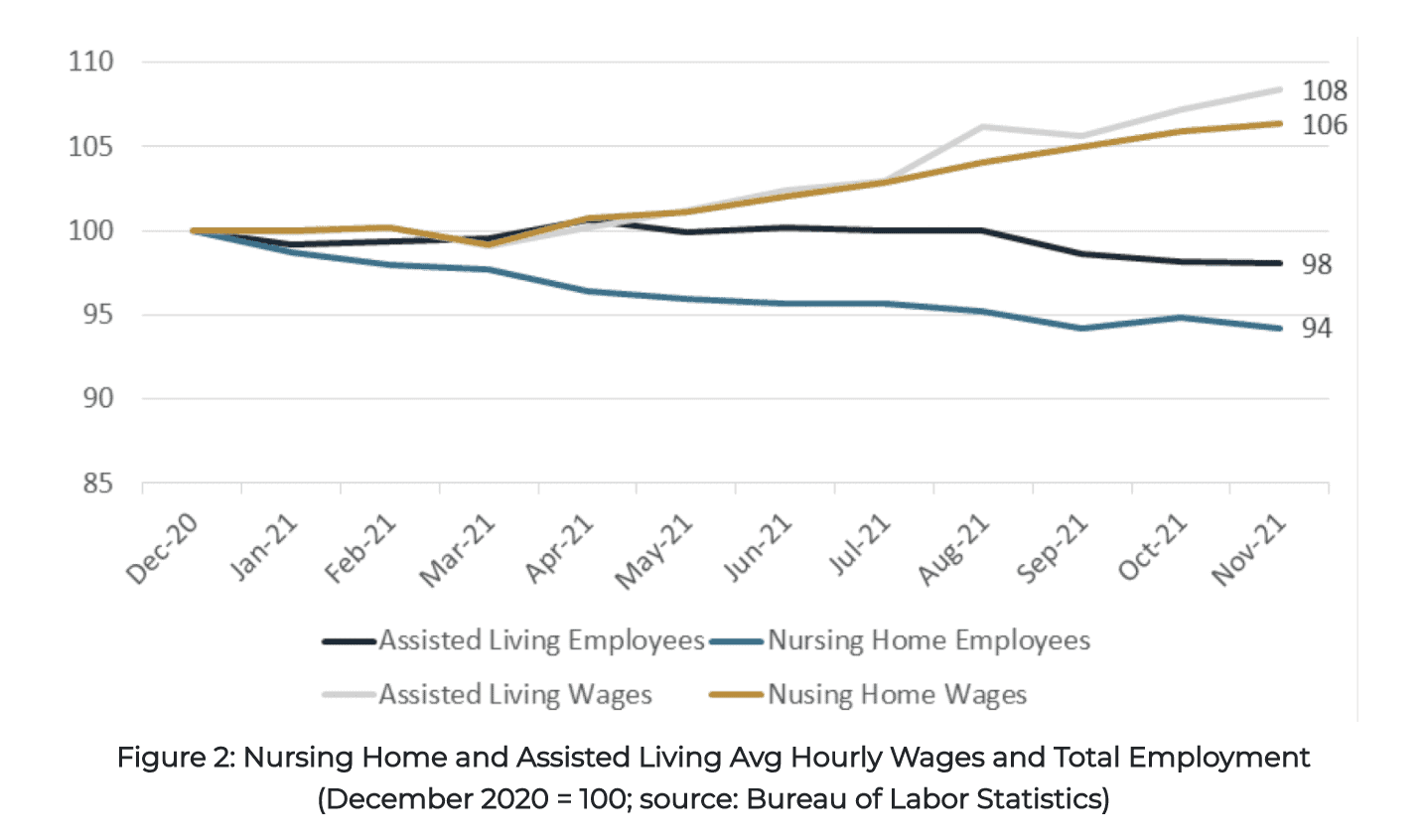

Challenges on the Labor Front

In addition to the issue of property performance, the seniors housing and care sector faces a separate but equally massive challenge in staffing. Many operators were reporting higher labor costs in 2021 due to a very competitive labor environment. Data from the Bureau of Labor Statistics (BLS) shows that assisted living and SNF wages grew in 2021 while the number of employees declined. This has undoubtedly led towards greater use of higher priced contract labor as new beds and units become occupied.

Transaction Volumes Pick Up

While transaction volumes pulled back in 2020 during the pandemic, they showed signs of returning to normal levels in 2021. The NIC/RCA Transactions Report shows that seniors housing transaction volume for the nine months ending September 30, 2021 was $10.1 billion, up 110% from the same period one year ago. For the SNF sector, transaction volume was $3.8 billion, up 81% from $2.1 billion one year ago.

Pricing Remains Strong

Mike Hargrave

Ventas boasted the largest transaction of the year through 3Q21, acquiring New Senior Investment Group for $2.3 billion in September 2021.

We might expect cap rates to be choppy in 2022. There is plenty of capital chasing seniors housing and skilled nursing assets which should mitigate perceived risks. Interest rates, which are forecast to rise in 2022, may impact exit cap rate expectations and the price investors are ultimately willing to pay for assets.

Those best positioned for success will be sure to stay on top of emerging trends throughout 2022 and collaborate with experienced partners to take advantage of market opportunities and navigate around potential risks.

Orin Parvin

Mike Hargrave is principal at Revista, and Orin Parvin is a director and deputy chief underwriter of the FHA LEAN program at Lument.